Fertilization

Litton Industries Inc., Annual Report, 1957.

“the influence of electronics is certain to be felt during the next decade, either directly or indirectly, by virtually every element of our national economy.”

“changes in the requirements in order to have the most advanced possible military force-in-being have brought about a shift in the character of procurement. Electronics is to be increasingly more important in the defense weapons of the future.”

“Many products which are not considered related to electronics today will feel the impact of the science in the future. Some industries may see the whole character of their products change, while others, of course, will be much less affected.”1

In 1957, Litton’s founder felt the winds of change swirling. As top-down institutional procurement departments renewed their investment locus, Charles Thornton’s company was perfectly positioned to benefit.

Working capital close to tripled. Earnings rose nearly 80%. The backlog almost doubled.

This was the year Henry Singleton was promoted to Director of the Electronics Equipments Division at Litton. Did his competence show in the numbers?

Summary Stats:

1957 Sales: $28,130,603

1956 Sales: $14,920,050

1957 Earnings $1,806,492

1956 Earnings $1,019,703

1957 Earnings per share $1.51

1956 Earnings per share $0.97

1957 Net Working Capital $6,731,956

1956 Net Working Capital $2,655,003

1957 Backlog $54,000,000

1956 Backlog $35,000,000

1957 Employees 2,700

1956 Employees 2,000

1957 Shareholders 4,500

1956 Shareholders 3,000

Calibrated Innovation

Studying Teledyne and Litton reminds us that innovation, value orientation, and growth can coexist.

“Value” investors might pose such a question:

How is it possible for a company to capture economic profits in technology when there is a diminishing marginal cost of reproduction (cheaper for competitors to imitate you), an incentive to disseminate products as widely as possible (more competitors can imitate through first principles), and constant change (difficult to forecast)?

Well … not all technology exhibits the second assumption of that question, as Charles Thornton showed us in 1957.

Even though products can be broadly applicable to many markets…

“The company’s 1957 catalog of transformer products lists over 75 models new to the company. Most of these new products have application in both military and commercial markets.”2

…monopolies can still exist:

“At mid-year, a new item of equipment of Litton Industries design, for which the company is the principal source, was put into production for still another of the nation’s important guided missiles.”3

In the twenty-first century, a lot of noise is made about raising outside capital, delaying gratification for decades, and aggressively pursuing market share at the sacrifice of present profits (for more in the future). Intuitively, if one understands compounding, such a strategy appears rational.

But such an approach seems ludicrous for anyone with significant skin in the game. Howard Marks citing the story of the 6ft man crossing a river that is 5ft deep on average springs to mind. A tenet of capitalism is ownership. Other People’s Money destroys the crux of what makes capital, as a force for progress, work.

What if there was another way?

Singleton and Thornton present a model of profitable innovation. Value investors shun aggressive sales growth without a demonstrable increase in value-per-share for long-term investors. And rightly so. Henry and Charles, who were both known to never sell their shares, aggressively reinvested in new products and processes and captured the economic benefits of doing so.

In the early days, both Teledyne and Litton grew in sequence.

“The company’s increased proprietary research and engineering activities, expanded plant capacity and facilities, and the addition of highly-qualified personnel give promise of realization of our growth plans - growth not just for growth’s sake, but the logical sequel to the establishment of a broad and strong company.”4

There seems to be a “logic” of the corporation’s growth: it wasn’t, by any means necessary. Instead, areas of research, experimentation, and iteration were intentional. This is distinct from the immediate MVP, move fast and break things, iterate and adapt philosophy that tends to characterize ideas about young technology companies in the twenty-first century.

Inside-Out

In 1957, novel color cathodes inside communications systems resulted in various potential applications for display technology and integrated systems:

“A unique color cathode ray tube having outstanding potential in numerous industrial and military applications, the new tube makes possible display of radar information on the radar screen in more than one color, at the election of the operator, giving an added and most important dimension to radar viewing.”5

An obvious break from the past. Radar displays presented distinct objects that made each visible to the radar operator and showed that the items on the screen were different, e.g. friendly vessel vs enemy pilot.

Great minds go inside their subject matter. How do qualitative investors go inside the companies they study?

At the heart of innovation is human creativity. In the same way that decisions are the fundamental building blocks of markets, humans are the building blocks of exceptional companies.

Even when Charles is explaining a step-change in Litton’s product offering, look at what he says produced that:

“In our inertial guidance activity, the feasibility of utilizing two-degrees-of-freedom gyros in inertial guidance systems was positively demonstrated by the company this year. For some years Litton Industries scientists have pioneered this revolutionary concept. Proof of its feasibility now makes possible inertial guidance systems more accurate, lighter in weight, and cheaper in cost than other inertial systems previously developed in the industry.”6

People are essential during product creation (engineering) and product acclimatization (sales) by enabling the market adoption of new products via effective sales organizations. Investors are often enamoured by new products or services and unintentionally disregard what is more difficult to see. It’s human nature. Peter Thiel argued that the importance of sales functions to a technology company’s success is often underestimated by investors.7 Thiel’s contrarian supposition fits with the emphases of Litton’s early annual reports:

“During the year, a new and expanded organization for the sale of the company’s precision components was established. More than 20% of our component sales came from products which were new this year.”8

That was 1957. Look at the Triad acquisition announcement in 1956:

“The addition of Triad’s outstanding and nationally known line of electronic transformers, wave filters, and other magnetic component products, represented throughout the country by 387 jobbers, distributors, and representatives - one of the most extensive sales organizations in our industry - will make a major contribution to our progress in the future.”9

Bottom-Up Analysis of Top-Down Decisions?

“Changes in the requirements in order to have the most advanced possible military force-in-being have brought about a shift in the character of procurement. Electronics is to be increasingly more important in the defense weapons of the future.”10

At the end of the 1950s, as Thornton alluded to, the U.S. Department of Defense redirected its spending. Initially, there was investment in the Air Force before funding trickled down to other areas of the military. A primary focus was electronics.

The cynic might ask why is a bottom-up analyst interested in markets governed by exogenous economic forces outside their control.

“The Secretary of the Air Force has recently indicated that by 1960 Air Force purchases of advanced electronic equipment and systems will have increased to approximately $1.3 billion a year as compared to 1956 purchases which totalled $756 million.”11

That is just under double in four years. Using the Rule of 72 implies (roughly) a 20% CAGR in institutional investment into military systems in the late 1950s. Not as high as one might expect given the extraordinary performance of Litton in 1957 which saw its earnings per share increase by 59.34%.

So we have the government spending more on electronics. What else contributed to Litton’s exceptional business performance?

The pattern of Henry Singleton’s early acquisitions at Teledyne revealed the extent to which holistic technological systems can be redefined and improved by replacing their underlying electronic components. That’s what your author terms combinatorial fructification.

Are some levels of technology more impactful than others?

Brian Arthur argues that technology has a recursive structure.12 At each level of the technology, you see a combination of other technologies below and above it. It’s a little abstract so let’s use an example.

Charles Thornton gives a perfect one:

“Included in missile procurement will be navigation, guidance, computing and control, instrumentation, and other equipment of the types developed and produced by Litton Industries.”13

On the surface, we see missiles. Underneath, families of different technologies co-exist and interrelate like telemetry, transducers, and potentiometers to name just three.

The point is not that each technology is identical or even its relationship to other technologies is similar at every level but that its structural form is self-similar from the inside out.

Perhaps then new technology at the most fundamental level of broader integrated systems would result in the largest second-order improvements in the holistic technological systems.

Petered Plans?

Singleton’s preference for flexible strategies and his distaste for plans is well known.

There is a clear distinction between Singleton’s philosophy (expressed in the 1980s) and Litton’s actions in the 1950s:

“The progress of an electronics company must be measured by its capability to envision future markets and opportunities, realistically plan and implement those plans, and accomplish the longer range objective of being a strong company recognised as a leader in a major industry - an industrial citizen that adds strength to national defense and to our national economy.”14

Singleton and Thornton practised opposite strategies. One could look at the long-term performance of Litton vs Teledyne and conclude flexibility is the “best” approach. But concluding that one is better than the other with no context lacks nuance.

Notice that Singleton commented in the 1980s whereas Charles Thornton was writing in the late 1950s.

If we rely upon the memory of George Roberts then we may believe that Henry also kept things flexible in the early acquisitive 1960s. That message rings loud and clear in George’s memoir Distant Force.

George Roberts joined Teledyne in 1966, with the acquisition of Vasco Metals. How can someone remember (with veracity) what a company was like before they joined?

Who Cares?

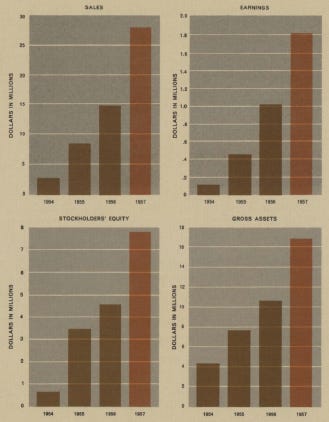

Teledyne and Litton’s annual reports have similar formats. Both report four key operational metrics in graphical form. Perhaps this was the corporate flair of the day?

Litton presented the following:

Sales

Earnings

Stockholders’ Equity

Gross Assets

Whereas Singleton presented these stats, in 1963:

Sales

Net Earnings

Working Capital

Shareholders’ Equity

The order of the presentation and specific items are similar but also slightly different. Singleton placed more emphasis on liquid assets and earnings excluding one-time benefits.

In contrast, a point of commonality is that both Litton and Teledyne displayed their key operating statistics from the inception of the company to the present day. Perhaps this is more common with founders who enjoy viewing the development of the figures over decades, not years.

On Laboratories: Geographical Dancing

“In cooperation with the Air Force Office of Scientific Research, the company has developed a unique research facility for the study of physical phenomena in an environment which simulates the conditions of ultra-high altitudes - altitudes currently far beyond the access of manned aircraft.”15

Above, Thornton mentioned the importance of high-quality people (an intangible asset). Tangible assets were central to his philosophy, just like Singleton:

“The Laboratory will facilitate research activity in the development of equipment that will operate in outer space. It is the only such laboratory existent in the free world.”16

“We attach significant importance to the extensive fund of basic scientific knowledge which the company has and will acquire in the operation of this facility. The culmination of over three years of effort, the continued success of the laboratory is destined to further enhance the company’s reputation in this new field.”17

Notice the importance of reputation. Litton’s focus on reputation was visible in a quote we discussed earlier too:

“The progress of an electronics company must be measured by its capability to envision future markets and opportunities, realistically plan and implement those plans, and accomplish the longer range objective of being a strong company recognised as a leader in a major industry - an industrial citizen that adds strength to national defense and to our national economy.”18

In Episode #110 of Founders, David Senra argues that many of the most successful entrepreneurs in history were avid teachers of their philosophies.

Again, we see Litton reiterating its plans for plant facilities and emphasising how this will benefit the company:

“Construction was begun on the first building of a new three-unit plant in Salt Lake City and plans are also being finalized for building a major addition to the new plant in San Carlos, California, for the Electron Tube Division. The capacity of this projected plant will be double the capacity of the division’s new plant completed and occupied in the fall of 1956.”19

The theme of combinatorial fructification can also be applied to physical locations and assets. By substituting and combining facilities that originated from different companies, the conglomeration is more productive, efficient, and valuable than the sum of the parts.

Teledyne used the strategy of combinatorial fructification in its early days. Did Henry learn that at Litton?

“Utrad, with a product line of pulse transformers complementary to that of Triad, also serves as an eastern manufacturing and distribution facility for certain of Triad’s product items.”

Though a theme of Teledyne was decentralization with empowered leaders at each level of the company, Litton displayed the opposite theme in 1957:

“The manufacture of our precision potentiometer line was centralized in one location in the East, and was expanded during the year. In the face of highly competitive market, continued highest quality production resulted in sales of this line being almost triple last year.”

Subsidiaries:

Here is a list of every wholly-owned Litton Industries company in 1957 (I wish Teledyne did this):

Litton Industries of California

Litton Industries of Maryland, Inc.

Triad Transformer Corporation

U.S. Engineering Co., Inc.

USECO, Incorporated

Utrad Corporation

The Automatic Seriograph Corporation

Majority Owned

West Coast Electronics Co. (99% of common & 85% of the preferred stock).

Earlier we touched on the emphasis Thornton placed on the sales organization of Triad in his announcement to shareholders.

Singleton and Thornton introduced their significant acquisitions in different ways. Litton describes what Triad excelled in at the time, and why it led the market:

“One of the nation’s leading producers of electronic transformers reactors, toroid coils, electronic wave filters and related products in wide use today in such advanced electronic equipment as guided missiles, commercial airline weather detection radar, communications systems, military fire control equipment, electronic computers, high fidelity sound systems, and precision electronic instruments. Triad also is one of the industry’s foremost firms in the design and manufacture of miniature and sub-miniature transformers for use with transistors.”20

Contrast that with Singleton’s description of how UED came into being and why it was at the forefront of a given market. As discussed in the Teledyne Inc. Annual Report 1964 write-up, Henry was an assiduous history student:

“In 1956 UED made the first application of solid state circuitry to airborne telemetry in the Sergeant missile program, and since that time has been a leader in advancing the technology of airborne telemetry.”21

Of course, Singleton didn’t always present acquisitions like this.

UED (Teledyne) and Triad (Litton) were important acquisitions made four years after Singleton and Thornton founded their electronics companies. Both were large and important to the company’s operations at the time. In Singleton, in Teledyne’s earliest annual reports, introduced key acquisitions just like Thornton did in the Litton annual reports. Simple. Straight to the point.

But as both companies grew and made selective acquisitions their presentations to shareholders changed.

Jim Nisbet’s 12th Question:

12. How is depreciation counted and is it a significant % of profit?22

Litton detailed their use of the Straight Line and Declining Balance methods in the 1957 Annual Report’s notes. (Such disclosure by a defense company in the mid-twentieth century was rare).

The straight-line method is well understood. This is simply taking the difference between the purchase price of an asset and its estimated terminal value over a certain number of years and decreasing its carrying value on the balance sheet by an equal amount each year.

The declining balance method front loads the decrease in an asset's carrying value. Think linear vs exponential decay. It also reduces the entire value of the asset down to zero whereas the straight-line method reduces the asset’s carrying value to a terminal value.

With the high rate of asset obsolescence in technology, it makes sense to use the declining balance method. But without knowing companies use(d) that method for certain, it would be dangerous to assume so.

In 1957, Litton’s depreciation charge was $694,000 against an operating profit of $3,530,739 and long-term assets (less accumulated D&A) of $5,338,231.

Therefore, Jim Nisbet looking at this company would focus on the 19.66% of operating profit charged as depreciation.

In isolation, that statistic means little. What is the ratio of declining balance to straight-line depreciation? I don’t know.

How does it compare to industry peers? This is where things get tricky.

Let’s look at Teledyne’s first public annual report.

In 1961, the total value (at cost) of Teledyne’s long-term assets was $1,049,586. They were carried at a net value of $649,766.

You need to remove the construction in progress figure of 65,332 because how can you depreciate physical assets that don’t exist?

Assuming the leasehold improvements have taken place on finance leases, whereby the assets accrue to the lessee at the end of the contract, there is a total cost of assets to be depreciated of 984,254 vs net long-term assets of 584,434.

That gives what appears to be a depreciation charge of 399,820 in 1961 alone. That figure over the 984,254 assets implies a 40.62% depreciation rate (if the straight-line method is used). Teledyne did not reveal in its notes which depreciation method it used.

Teledyne’s EBIT was $144,795 in 1961! A depreciation charge of $399,820 over $144,795, i.e. depreciating more than double operating profit. Not quite.

Teledyne acquired assets from companies that had accumulated depreciation from years before 1961 so what looks like a double-operating-profit depreciation charge doesn’t measure depreciation charged in 1961 alone but many years beforehand too.

You could try to figure out depreciation from first principles. This might work by looking at the change in accumulated depreciation over several years. However, you run into difficulties because of the additional acquisitions that occur year after year at Teledyne.

The media labelled Henery Singleton the sphynx. His ability to say a lot with little was evident also in Teledyne’s annual reports.

Dear Intelligent Investor,

Thank you for reading.

You can access this report and more due to the generosity of Adam Mead here:

Charles Thornton, Litton Industries, Annual Report 1957. pp. 4-5.

Litton (1957), pg. 20.

Litton (1957), pg. 18.

Litton (1957), pg. 2.

Litton (1957), pg. 8.

Litton (1957), pg. 16.

Peter Thiel with Blake Masters, Zero to One (2014), pg. 21, and pp. 126-130.

Litton (1957), pg. 20.

Charles Thornton, Litton Industries, Annual Report 1956, pg. 6.

Litton (1957), pg. 4.

Litton (1957), pg. 4.

Brian Arthur, The Nature Technology: What It Is and How It Evolves (2009), pp. 37-43.

Litton (1957), pg. 4.

Litton (1957), pg. 5.

Litton (1957), pg. 12.

Litton (1957), pg. 13.

Litton (1957), pg. 12.

Litton (1957), pg. 5.

Litton (1957), pg. 10.

Litton (1956), pg. 8.

Henry Singleton, Teledyne Inc. Annual Report 1964, pg. 12.

James Nisbet, The Entrepreneur (1976), pg. 148-149.

This is excellent! Out of curiosity where did you track down the report?