A Pilgrim's Progress

A Pilgrim's Progress

Litton Industries, Annual Report 1958.

In the 1958 Litton annual report, there are 16 pages of written MD&A (shareholder letter included). The word “progress” is used 13 times.

Charles B. “Tex” Thornton’s Highlights

1958 Sales: $83,155,473

1957 Sales: $28,130,603

1958 Earnings: $3,702,203

1957 Earnings: $1,806,492

1958 Net Working Capital: $23,117,831

1957 Net Working Capital: $6,731,956

1958 Employees: 8,600

1958 Employees: 2,700

1958 Common Stockholders: 5,801

1958 Common Stockholders: 4,500

Notice that Tex has removed backlog, an essential metric for equity investors estimating predictability, from his operational highlights. Why?

Diversification inside Concentration

“Litton Industries has been organized as a company with a product base rooted in new technology and with a plan for projecting its technological advances into diverse market areas.”

If you bring up the idea of investment screens to experienced investors, sometimes, their noses transform from an asparagus’ base - straight and rigid - to its tip - scrunched - in a split second. “Our investment universe is quite narrow.” The implication is that screens can’t measure qualitative elements well.

Nick Sleep’s thinking implies that the utility of screens in investment ideation depends on the screener, not the screen:

“Quality of managerial character is therefore important to avoid capital misallocation and it is in the search for such character that we asked an investment bank to perform a simple company search earlier this year [2003]”

“The criterion was for companies with no increase or decrease in shares outstanding in the last ten years.”1

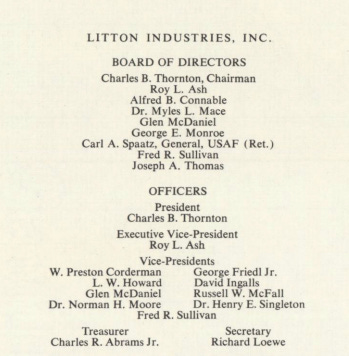

In Litton’s 1958 annual report, the first thing that stood out to your author was the number of names on Litton’s board of directors.

Charles B Thornton

Roy Ash

Glen McDaniel

Fred Sullivan

9 board members. 13 Officers. Notice that ~44% of the board are officers at Litton. ~31% of the officers are board members.

Compare that to Teledyne, in 1965:

Henry E Singleton

George Kozmetsky

Robert B Sprague

5 board members. 10 officers. Notice in this case 60% of the board members are officers. 30% of the officers are board members.

Subtle differences that probably mean nothing…

It’s not the specific number on the board that is important (or is it?). What ideas would a screen today produce for companies with boards half the size of the average in their industry?

James Nisbet attributed Teledyne’s lean, decentralized structure to the company’s youth:

“Older companies such as General Electric tend to shift in degrees of centralization like a pendulum - swinging too far in centralizing by one president and then too far in decentralizing by another…

A new company like Teledyne, however, is not yet mature enough to have developed an office filled with a corporate staff… The point was that experts on Teledyne’s staff didn’t exist.”2

Youth was not the cause.

In both cases, these boards existed five years after the founding of the companies in their latest form. Tex formed Electro Dynamics Corporation in 1953 and acquired the assets of Litton Industries in 1954 from the founder Charlie Litton. Over the same duration, Litton built up to nine board members, while Teledyne kept only five.

Succulent Sales, Memetic Marketing

“The years ahead hold unusual opportunities for those companies that have a broad capability for competent research, can design and produce economically useful products, and can effectively market the ever-improving products of their research and manufacture.”

In 1958, Tex was still leading with the earnings statement in his presentation to shareholders. Any guesses as to why?

“On January 15, stock of the company was exchanged for 100% of the outstanding stock of Monroe Calculating Machine Company. The merging of the two companies brought to Litton a network of 325 sales and service branches in the United States, three manufacturing plants… More than 2000 sales and service personnel in the field, representatives of the 47-year-old line of Monroe business machines, have already added Litton Industries to their identification.”

Tex’s goal was to have $100 million within 5 years of his company’s founding. An arbitrary round number plucked from thin air? Acquisitions were an efficient way to get closer to that goal in 1958:

“[Monroe] needed Litton’s fine technological assets for further growth… in return for which Tex would benefit from our extensive sales and service outlets and would save a heck of a lot of time carrying out his plan to penetrate commercial markets…

Even after these acquisitions, plus continued internal growth, Thornton had still not reached his spectacular goal at the end of Litton’s fifth fiscal year, on July 31st, 1958 - sales were up to $81 million.”3

Tex alluded to the historical context behind Monroe in those quotes but his priority was the sales function of the organization more than the technological prowess.

The quantity of sales was important to Litton. Tex’s company was the progeny of U.S DoD spending, but his vision was much broader. He desired to disseminate technology as widely as possible. In other words, quality mattered too:

“Even more significant, however, was the change that took place in the nature of the sales. From an approximate relationship of 85% military - 15% commercial, sales this year were approximately 45% military and 55% commercial.

The element of acquiring sales and marketing infrastructure was behind the Westrex transaction too:

“The acquisition of Westrex added to the Litton marketing structure a distribution network of 35 sales and service branches covering 50 foreign countries. This organization now enables Litton to provide experienced sales and service capability in the foreign field for the many products which the company had already begun to market there.”

Teledyne inverted Litton’s outsourced marketing strategy:

“We also began the development of our own in-house advertising agency…

We created a separate Teledyne company named TRL Productions (Teledyne Republic Lakeland)...

TRL placed advertising for some 80 Teledyne companies over the years, and saved a substantial amount of money.”4

That was in 1977. Teledyne was a different garden to the one it was in 1965. Of course, the context of that decade was different from that surrounding Litton in the late 1950s. So we’re not comparing apples with apples.

Interestingly, Singleton didn’t reveal a marketing strategy in Teledyne’s earliest annual reports. However, the aggressive pursuit of primary supplier status on complex systems and inertial guidance contracts was a marketing strategy in and of itself, whether it was labelled as such or not.

This contrasted with Charles Thornton’s more cautious approach:

“Litton is one of the few corporations that does not have any international division for marketing at the corporate level.

Prudence entered into his early game plan when he elected to stay away from bidding on complete “systems” for the Department of Defense or NASA, although he was systems-minded from the first. It made more sense, until Litton grew bigger, to be a subcontractor to the prime contractor who bore financial responsibility, with the added advantage of using government R&D money to develop expensive new products and components which would have later commercial applications, and which would provide invaluable experience for more ambitious contracts later.”5

John as Tex Thornton’s Malone?

A line in the Litton report revealed that Tex Thornton delineated cash and non-cash expenses in a way that is commonplace today but was rarer at the time.

Look at his analysis of Litton’s resources:

“Cash generated for reinvestment in the company (net earnings plus depreciation) exceeded $5.6 million, making a major contribution toward our continued growth.”

This has a whiff of EBITDA. John Malone is celebrated for coining this term to investors and popularising it in the 1970s. Almost 20 years after Tex’s beginnings at Litton.

Wherecraft?

Thinkers with an affinity for logical reasoning classify and delineate concepts due to their essence. This can be a strength and a weakness: first principles thinking is natural but dichotomous thinking can also abound.

In the context of Litton’s annual report, your author previously commented on the trickle-down effect in the late 1950s: the U.S. Department of Defense shifted its concentration of funding to electronics in the Air Force. One might think that the Air Force was involved with all technology that improved flight experience. Not the case.

In 1958, several aircraft projects were cited in Litton’s report. Many emanated from the Navy.

“The company has for some time had the prime responsibility for development and manufacture of an airborne data processing and display system for use in Navy’s principal early warning aircraft.”

“Currently under development are display control computers for military helicopters, guidance and control computers for a Navy advanced all-weather attack aircraft and computers for a satellite reconnaissance installation now in the advanced planning stage by the military services.”

As we’ve discussed before, there exists a first-mover advantage in military contracts. Think of a bubble: incubated network effects with increasing returns. The more military programmes one supplier wins, the more likely they are to use the same supplier for another contract that needs technology to connect or interact with the previous contract.

“Progress made to date has resulted in the company receiving contracts to develop and produce related systems for other naval applications and for ground installation use by the Marine Corps.”

The Littonic Diaspora

Combinatorial fructification of similar business units as well as acquisitions with stock were two corporate strategies implemented by Litton.

Is your author falling for the anachronistic fallacy by insinuating that Henry Singleton’s strategy of combinatorial fructification was evident at Litton?

We’ve touched on the two kinds of combinatorial fructification before. One was Henry’s planting of microelectronics inside complex and inertial guidance systems. The second was the recomposition of physical assets from various separate companies to create unique tangible and intangible assets for a new whole under Teledyne.

Did Singleton learn the second type from Thornton’s combination of two plants that were similar and geographically close in 1958?

“The newly acquired Maryland Electronic Manufacturing Corporation with Litton Industries Maryland Division was underway. Blending together the two groups, engaged in complementary field of work, was simplified by the fact that the two plants are located adjacent to each other in College Park, Maryland. The combined plant area now covers over 135,000 sq. ft., and a 35,000 sq. ft. addition is currently under construction.”

“Seven months later, the rate of shipments had increased substantially for the combined operations and 50 per cent more people were on the division’s employment rolls.”

Henry learnt the mindset and execution skills at Litton from someone with a background in statistics. When Singleton combined that with his prowess in science and technology, something special occurred.

So far the following three themes are evident in Thornton’s and Singleton’s philosophies:

Frugality

There are two similar stories of both Singleton and Tex being extremely frugal with company cars that make me laugh:

“One of his vice-presidents brought back a flashy-looking Jaguar sports car from Europe. Tex was appalled.

“Man, you must be crazy,” he said. “Don’t ever park that thing around here again. What would people think?”

The executive got rid of the Jaguar. And Tex continued to drive his Ford to work.”

“Henry never felt that luxury automobiles were a necessity at any facility. In fact, at one point Henry suggested that Ford Pintos be used for company cars at all facilities. This caused a bit of a problem when Jim Steitle and four of his staff (they were all big men in the 6’5”, 250-pound class) tried to squeeze into a Pinto. It was an impossible task.”6

Broad Directions

“To Tex the move was a logical extension of his philosophy of thinking under broad headings rather than in terms of products.”7

That is exactly how Singleton viewed his early acquisitions in the early 1960s. Individual companies were building blocks of human and technological systems that - when combined - brought Teledyne closer to its long-term objectives of leadership in integrated circuits and primary contractor status.

Autonomy

“Tex gave me a lot of autonomy but you always knew who was boss. He believed in the homely values of hard work, but he didn’t care whether you were on the job all night or only half a day as long as you got results.”8

Teledyne’s decentralized structure empowered management teams at the local levels. Buffett imitated that, at Berkshire.

So, to what extent did Henry learn from Tex? What about other senior leaders at Litton… what did they go on to achieve?

“None of the others has gone as far, as fast, and on as straight a course as Tex… he’s definitely set the pace and most of the others have learned from him and paid him the sincerest compliment of imitation.”

“Tex does not give the impression that he is particularly upset by having presided, in effect, over a graduate school for corporate presidents who in most cases have paid him the compliment of feverishly imitating his methods, especially in the realm of acquisitions.”9

Outside Looking-In Statistics

1958 Gross Margin: 45.85%

1958 EBIT Margin: 9.41%

1958 ROE: 13.22%

1958 ROA: 6.51%

1958 Capital Turnover: 3.0

1958 Working Capital Turnover: 5.6 (after deducting pref. & common dividends)

1958 Inventory Turnover: 3.3, which implies 110 days to sell their products.

No depreciation charge was shared in the notes this year. Depreciation as a % of operating profit was too difficult to calculate via induction due to several acquisitions.

Dear Intelligent Investor,

Thank you for reading.

You can access this report and more due to the generosity of Adam Mead here:

RIP Charlie.

Some Excellent Thinking

Nicholas Sleep & Qais Zakaria, “Nomad Investment Partnership Letters to Partners 2001-2014”, pg 21.

James Nisbet, The Entrepreneur (1976), pg. 164.

Beirne Lay, Someone Has to Do It (1969), pg. 148.

George Roberts, Distant Force (2007), pg. 155-156.

Lay, Someone…, pp. 146-164.

Roberts, Distant…, pg. 41.

Lay, Someone…, pg. 163.

Lay, Someone…, pg. 148.

Lay, Someone…, pp. 160-161.